Debt and equity securities classified in Degree 1 of the truthful value hierarchy are valued utilizing prices quoted in energetic markets for those securities. Debt securities categorised in Stage 2 of the fair worth hierarchy are valued using a matrix pricing method. Matrix pricing is used to worth securities primarily based on the securities’ relationship to benchmark quoted costs. Commercial and residential mortgage-backed securities categorized in Level three are valued using discounted money move methods. Collateralized debt obligations classified in Level three are valued utilizing consensus pricing.

Valuation Strategies

You ought to consult with a certified skilled advisor about your specific scenario before undertaking any action. That’s why we ship quickly, sometimes in as little as one business day, and explain results in plain language so they’re not simply technically correct, but additionally useful in your team. Eton brings the experience and technical depth wanted to make sure valuations are correct, defensible, and introduced clearly. The CSE method assumes that each one most well-liked shares convert into frequent stock, which is strictly what occurs in an IPO. This methodology distributes value primarily based on the rights and liquidation preferences of every share class.

The legal responsibility would not be settled with the counterparty or otherwise extinguished on the measurement date. Market individuals with whom the entity would enter right into a transaction in that market. In the absence of a principal market, in probably the most https://www.simple-accounting.org/ advantageous marketplace for the asset or legal responsibility.

5Three Equity Securities – Disclosure Necessities

Assumptions concerning the highest and finest use of a non‑financial asset shall be constant for all of the belongings (for which highest and finest use is relevant) of the group of belongings or the group of assets and liabilities within which the asset can be used. Though an entity must have the ability to entry the market, the entity doesn’t want to be able to promote the actual asset or switch the actual legal responsibility on the measurement date to have the power to measure honest worth on the premise of the worth in that market. This kind consists of nine actual property funds that make investments primarily in U.S. business actual estate. The truthful values of the investments in this kind have been determined using the NAV per share (or its equivalent) of the Plan’s possession curiosity in partners’ capital. Distributions from every fund might be acquired as the underlying investments of the funds are liquidated.

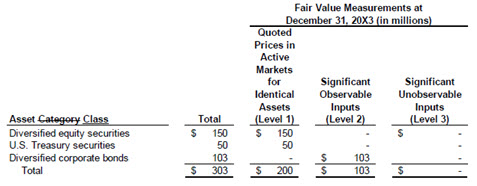

- Stage 1 inputs are quoted costs (unadjusted) in energetic markets for equivalent assets or liabilities that the entity can entry at the measurement date.

- These assumptions are called unobservable inputs, since they can’t be verified in opposition to market activity, which makes Stage 3 valuations essentially the most subjective.

- As A End Result Of investing is a key part of the plan’s activities, the plan reveals larger disaggregation in its disclosures.

- Whether the liability is an obligation to ship money (a monetary liability) or an obligation to deliver items or services (a non‑financial liability).

- By addressing these challenges and issues, entities can improve the reliability and credibility of their fair worth measurements, offering stakeholders with a real and fair view of their monetary position and efficiency.

This publication will assist you to apply the principles of ASC 820 and IFRS thirteen Fair Worth Measurement and understand the key variations between the accounting requirements. We discussed the assets eligible and required to be reported at honest worth, including financial assets, investment properties, biological assets, and sure intangible property. We additionally lined the varied fair worth measurement techniques—market method, income method, and cost approach—and supplied examples of how every technique is applied. In some cases, the inputs used to measure the honest worth of an asset or a legal responsibility could be categorised within totally different ranges of the truthful value hierarchy. In these circumstances, the truthful value measurement is categorised in its entirety in the identical degree of the truthful value hierarchy because the lowest stage input that’s vital to the entire measurement.

An entity could additionally be required to allocate a good worth measurement when the unit of account for the merchandise measured at honest worth differs from the unit of valuation. In some circumstances, an allocation will be required even when the unit of account and unit of valuation are the identical. Under ASC 820, it is assumed that an entity will transact in its principal market or, within the absence of a principal market, the most advantageous market. This willpower is important as a end result of exit costs are not the same in different markets. In most conditions, there might be a principal market, which represents the market with the greatest volume and level of activity for the merchandise.

The aim is to provide anybody relying on financial statements a clearer image of how much confidence they’ll place in a reported fair worth. Beyond defining fair worth, ASC 820 additionally explains how to decide the quality of the inputs used to measure it. This system known as the honest worth hierarchy, and it’s designed to make valuations extra transparent.

6Three Annual Summarized Monetary Information—equity Methodology Investees

This appendix sets out amendments to other IFRSs which are a consequence of the Board issuing IFRS thirteen. An entity shall apply the amendments for annual periods beginning on or after 1 January 2013. If an entity applies IFRS thirteen for an ancient times, it shall apply the amendments for that ancient times. Amended paragraphs are shown with new text underlined and deleted textual content struck by way of.

In contrast, the truthful value of the asset or legal responsibility is the value that would be received to sell the asset or paid to switch the legal responsibility (an exit price). Similarly, entities don’t necessarily switch liabilities at the prices obtained to imagine them. Corporations are dealing with a myriad of adjustments – including the rise of synthetic intelligence, transition to a greener financial system and new world taxes – in addition to uncertainties about geopolitical occasions, inflation and interest rates. Any of these issues might require corporations to reevaluate the judgments, inputs and significant assumptions underpinning their fair value measurements. Traders and regulators have been raising concerns concerning the clarity of monetary reporting, together with about measurement uncertainties. In occasions like this, it is important that companies tell a transparent story by providing clear disclosures.

However, using an alternative pricing methodology results in a fair worth measurement categorised within a decrease level of the honest worth hierarchy. In this easy illustration, the anticipated money flows (CU780) represent the probability‑weighted common of the three potential outcomes. Nevertheless, to apply the expected current worth method, it’s not always essential to keep in mind distributions of all potential money flows using complex fashions and strategies. Rather, it might be possible to develop a limited number of discrete scenarios and probabilities that capture the array of attainable money flows. When measuring the truthful value of a legal responsibility or an entity’s own equity instrument utilizing the quoted price for the similar item traded as an asset in an active market and that value must be adjusted for components particular to the item or the asset (see paragraph 39).